Markets Remain Unstable Amidst Encouraging and Concerning Economic Data

Week 15 | 10 - 14 April 2023

Last week's economic data presented investors with a mixed picture. Encouraging reports on the inflation front indicated a possible moderation in consumer prices after reaching 40-years highs over the past year. However, the latest retail sales report showed a faster-than-expected contraction raising concerns over a potential recession. Despite these developments, the combination of moderating inflation and a decelerating economy could prompt the Federal Reserve to end its aggressive rate hike cycle, a move that has historically had a positive impact on the stock market. On the other hand, the first quarter earnings season kicked off with reports from banking giants and will continue over the next few weeks. This week’s events suggest that the markets are still not stable and prone for continued volatility as we move forward.

Despite persistent concerns of a potential recession, the major benchmarks posted gains for the week. The Dow Jones Industrial Average (DJI) rose by 1.34%, the S&P 500 (SPX) increased by 1.42%, and the Nasdaq Composite (NDX) saw a gain of 1.18%.

From a sector perspective, financials were the top performers last week, fueled by better-than-expected earnings from major banks. Energy also outperformed, driven by OPEC+'s decision to cut production. Conversely, real estate lagged, weighed down in part by concerns about a potential recession and a further slowdown of the economy.

Inflation Eases in March

Last week, the Labor Department's release of the consumer price index (CPI) for March was highly anticipated, with stocks jumping on the news that the CPI rose only 0.1%, bringing the year-over-year rate to 5.0%, the slowest pace since May 2021. However, Federal Reserve Bank of Richmond President Thomas Barkin's comments that "there is still more to do" in calming inflation caused the indexes to fall back later in the day. The March CPI report revealed that inflation remains on its downward path, driven in large part by a drop in oil and food prices. While core inflation, which excludes volatile energy and food costs, rose as expected, putting inflation at a 5.6% annual rate, used vehicle prices fell sharply from the prior month and upward pressure from shelter costs eased. However, elevated services prices persist, notably in the leisure categories such as hotels and airfare.

On Thursday, further encouraging inflation news on the producer side was reported, with the core producer price index declining 0.1% in March, marking the first decrease in the prices businesses pay for inputs since the height of the pandemic shutdowns in April 2020. Overall, while inflation remains above the Fed's 2% long-term target, the report suggests that better prices may be in the pipeline for consumers.

Retail Sales & Manufacturing Output Raise Recession Concerns

The week's data provided mixed signals about the state of the economy. On one hand, jobless claims rose slightly above consensus estimates, but remained below their levels in March, indicating a stable labor market. On the other hand, retail sales fell more than expected in March, mainly due to price cuts in some categories such as gasoline. Consumer spending is softening, with retail sales down 1% in March, led by declines in vehicle, building material, and gas station sales. The decline in retail sales raised concerns about the risks of a recession, even with the Federal Reserve considering another interest rate increase at its May meeting.

Here are the key metrics from the data:

Retail sales fell by 1% to $691.7 billion in March, worse than market expectations of a 0.4% decrease.

Excluding automobile sales, retail sales dropped by 0.8%, compared to analysts' forecast of a 0.3% decline.

Manufacturing output fell 0.5% from February and 1.1% from March of 2022.

Average capacity utilization fell 0.5% to 78.1%, less than one percent under the 50-year norm, indicating the post-COVID economy's instability.

Big Banks Score Strong Q1 Earnings Despite the Banking Crisis

The earnings season began on Friday as several large banks and firms announced their Q1 earnings. Despite recent industry crises, major US banks reported strong earnings due to higher interest rates and a growing economy.

JPMorgan Chase & Co's Q1 profits increased by 52%, with revenue up 25% YoY, surpassing Wall Street estimates.

Wells Fargo reported Q1 earnings of $1.23 per share, exceeding consensus by 11 cents, with revenue up 18% YoY.

PNC Financial reported Q1 earnings of $3.98 per share, exceeding consensus by 34 cents, with revenue up 19% YoY.

Citigroup's Q1 revenue was $21.4 billion, up 12% YoY and exceeding consensus by $1.34 billion. Its adjusted EPS was $1.86, beating consensus by 17 cents.

Europe sees gains as recession fears ease, China faces inflation concerns

Yields on 10-year government bonds in Germany, France, and the UK moved higher as investors evaluated the likelihood of more policy tightening by the European Central Bank. In economic news, Eurozone industrial production rose 1.5% sequentially and 2.0% YoY, while retail sales volumes fell 0.8% sequentially in March. The UK economy was on track to avoid a first-quarter recession, despite a flat GDP reading in February.

On the other hand, China's consumer price index rose by 0.7% in March from a year earlier, below the government's target of 3%, while the producer price index declined for the sixth consecutive month. The lower inflation figures raised expectations that the People's Bank of China (PBOC) could implement further monetary easing to support the economy, including a possible cut to the policy rate for its lending facilities. China's exports unexpectedly rose 14.8% in March from a year ago, surprising analysts who had forecast a decline, while imports fell less than expected.

Key Takeaway

Based on the current economic conditions, it is expected that any recession in the near future would be short and mild. This is because the labor market is currently in a good position, having enjoyed low unemployment rates and significant payroll and wage growth. Furthermore, the moderation of inflation is likely to enable the Federal Reserve to halt its rate-hiking cycle soon, with an additional quarter-point hike expected in May. This last potential increase might be driven by the Consumer Price Index (CPI) which is currently running over 5% above year-ago levels, which is more than double the Fed's long-term target. Yet, the anticipated pause by the Fed will be a critical condition for the market to establish the foundation for a sustained recovery. Although there might be a return of market volatility, the recent gains in the stock market are encouraging. The Fed's move to the sidelines is expected to provide an additional boost to the market's positive performance.

During this period, a well-balanced portfolio can outperform. One can achieve this by holding onto gold as a hedge against inflation and maintaining a mix of investment-grade bonds with shorter and longer durations. As we approach the Fed’s decision in early May, there may be volatility, so caution is key. Investors should view any market fluctuations as an opportunity to diversify and add quality investments that align with their financial goals. This could involve searching for high-quality stocks trading at a discount and monitoring the performance of current holdings.

Remember that market commentary, including this one, provides valuable insights and information, but the future can be different. To stay informed and make informed decisions, it's important to do your own research and stay up-to-date on market trends and developments.

The Week Ahead

Tuesday, April 18, 2023

Building Permits - March

Housing Starts - March

Wednesday, April 19, 2023

Crude Oil Inventories

Thursday, April 20, 2023

Initial Jobless Claims

Philadelphia Fed Manufacturing Index - April

Existing Home Sales - March

US Leading Index - March

Friday, April 21, 2023

Manufacturing & Services PMI - April

Corporate View

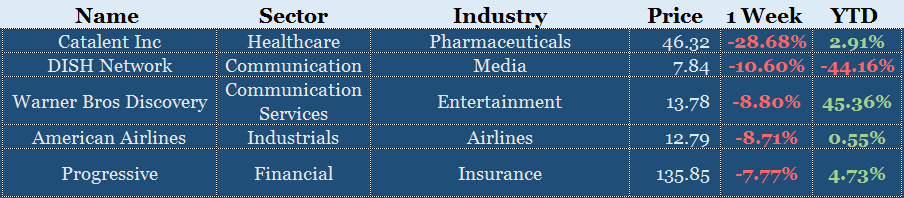

Weekly Top Performers

Weekly Worst Performers

Major Earnings Announcements 10 - 14 Apr 2023

Albertsons Companies (ACI): estimated $0.69, actual $0.79

Fastenal (FAST): estimated $0.49, actual $0.52

Delta Air Lines (DAL): estimated $0.29, actual $0.25

UnitedHealth Group (UNH): estimated $6.24, actual $6.26

JPMorgan Chase & Co. (JPM): estimated $3.41, actual $4.10

Wells Fargo & Company (WFC): estimated $1.15, actual $1.23

BlackRock (BLK): estimated $7.71, actual $7.93

Citigroup (C): estimated $1.66, actual $1.86

The PNC Financial Services Group (PNC): estimated $3.60, actual $3.98

Major Earnings Announcements 17 - 21 Apr 2023

Charles Schwab (SCHW): estimated $0.91

Johnson & Johnson (JNJ): estimated $2.51

Bank of America (BAC): estimated $0.79

Netflix (NFLX): estimated $2.81

The Goldman Sachs Group (GS): estimated $8.14

Tesla (TSLA): estimated $0.85

ASML Holding (ASML): estimated $4.59

Abbott Laboratories (ABT): estimated $0.98

Morgan Stanley (MS): estimated $1.67

Taiwan Semiconductor (TSM): estimated $1.21

Philip Morris International (PM): estimated $1.33

AT&T (T): estimated $0.58

American Express (AXP): estimated $2.66

Procter & Gamble (PG): estimated $1.32

You can check our website victoryinvest.co for further insights.